Assets are resources owned by a company as the result of transactions. Examples of assets are cash, accounts receivable, inventory, prepaid insurance, land, buildings, equipment, trademarks and customer lists purchased from another company, and certain deferred charges.

The term fixed assets generally refers to the long-term, tangible assets used in a business that are classified as property, plant and equipment. Examples of fixed assets are land, buildings, manufacturing equipment, office equipment, furniture, fixtures, and vehicles. Except for land, the fixed assets are depreciated over their useful lives

Depreciation

Since most assets depreciate in value overtime, accounting practices mandate that fixed assets are prorated to decrease their value on the books over an estimated period of time. Buildings, machinery, equipment, furniture, fixtures, computers, outdoor lighting, parking lots, cars, and trucks are examples of assets that will last for more than one year, but will not last indefinitely. During each accounting period (year, quarter, month, etc.) a portion of the cost of these assets is being used up. The portion being used up is reported as Depreciation Expense on the income statement. In effect depreciation is the transfer of a portion of the asset's cost from the balance sheet to the income statement during each year of the asset's life.

Depreciation expense

The income statement account which contains a portion of the cost of plant and equipment that is being matched to the time interval shown in the heading of the income statement. (There is no depreciation expense for land.)

Accumulated depreciation

The amount of a long term asset's cost that has been allocated to Depreciation Expense since the time that the asset was acquired. Accumulated Depreciation is a long-term contra asset account (an asset account with a credit balance) that is reported on the balance sheet under the heading Property, Plant, and Equipment.

The calculation and reporting of depreciation is based upon two accounting principles:

1. Cost principle. This principle requires that the Depreciation Expense reported on the income statement, and the asset amount that is reported on the balance sheet, should be based on the historical (original) cost of the asset. (The amounts should not be based on the cost to replace the asset, or on the current market value of the asset, etc.)

2. Matching principle. This principle requires that the asset's cost be allocated to Depreciation Expense over the life of the asset. In effect the cost of the asset is divided up with some of the cost being reported on each of the income statements issued during the life of the asset. By assigning a portion of the asset's cost to various income statements, the accountant is matching a portion of the asset's cost with each period in which the asset is used. Hopefully this also means that the asset's cost is being matched with the revenues earned by using the asset.

There are several depreciation methods allowed for achieving the matching principle. The depreciation methods can be grouped into two categories: straight line depreciation and accelerated depreciation.

The assets mentioned above are often referred to as fixed assets, plant assets, depreciable assets, constructed assets, and property, plant and equipment. It is important to note that the asset land is not depreciated, because land is assumed to last indefinitely.

Example

To illustrate depreciation used in the accounting records and on the financial statements, let's assume the following facts:

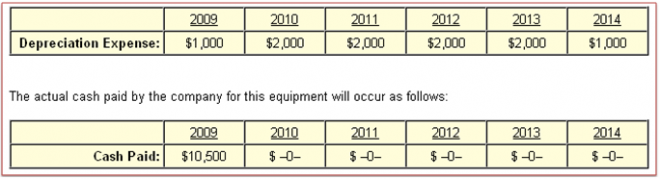

* On July 1, 2009 a company purchases equipment having a cost of $10,500.

* The company estimates that the equipment will have a useful life of 5 years.

* At the end of its useful life, the company expects to sell the equipment for $500.

* The company wants the depreciation to be reported evenly over the 5–year life.

Calculation of Straight-line Depreciation

The most common method of depreciating assets for financial statement purposes (as opposed to the method used for income tax purposes) is the straight-line method. Under this depreciation method, the depreciation for each full year is the same amount.

The depreciation expense for a full year when computed under the straight-line method is illustrated here:

Cost of the asset $10,500

Less: Expected salvage value – 500

Depreciable Cost (amount to be depreciated over the estimated useful life) $10,000

Years of estimated useful life 5

Depreciation Expense per year $ 2,000

If a company's accounting year ends on December 31, the company will report the depreciation expense on the company's income statement as shown in the following depreciation schedule:

What entry is made when selling a fixed asset?

When a fixed asset or plant asset is sold, the asset’s depreciation expense must be recorded up to the date of the sale. Next, 1) the asset’s cost and accumulated depreciation is removed, 2) the amount received is recorded, and 3) any difference is reported as a gain or loss.

Here’s an example. A company sells one of its machines on January 31 for $5,000. The last time depreciation was recorded was on December 31. Depreciation expense is $400 per month. The general ledger shows the machine’s cost was $50,000 and its accumulated depreciation at December 31 was $40,000.

On January 31 the company will debit Depreciation Expense for $400 and will credit Accumulated Depreciation for $400 in order to record the depreciation during January. In its next entry on January 31, the company will debit Cash for $5,000 (the amount received); debit Accumulated Depreciation for $40,400 (the balance at January 31); debit Loss of Disposal of Asset $4,600; and credit Machines for $50,000.

Let’s step back and review the disposal of the machine. As of January 31, the machine’s book value is $9,600 (cost of $50,000 minus its accumulated depreciation of $40,400). Because the asset is sold, the $9,600 of book value or carrying value is removed from the accounts. In its place, the company received and records the cash of $5,000. Since the company received $4,600 less than the amount it removed, it will report a loss of $4,600.

If the company had received more cash than the asset’s book value, it would report the difference as a credit to Gain on Disposal of Asset

0 comments