Encumbrances are obligations for future expenditures made to an employee or made to an outside vendor. Encumbrances are tracked to help departments forecast their expenditures so that they do not exceed their budget available.

In business, an encumbrance is created when a Purchase Order is issued to buy goods or services. The money has not yet been spent, but is "earmarked" for that purchase and no one else can use it. In real life, if you put money into an envelope to hold it to pay a bill, you have encumbered that money. You probably don’t use budget codes, but if you have an envelope in your dresser drawer marked “ELECTRIC BILL”, the money you stash away for the next bill is your encumbrance. How much should be encumbered? How much do you THINK your bill is going to be? That’s the encumbrance.

The primary purpose of tracking encumbrances is to avoid overspending a budget. Encumbrances can also be used to predict cash outflow and as a general planning tool.

To use the full capabilities of encumbrance accounting, you must enable the budgetary control flag for a set of books. When you enable the budgetary control flag, the system automatically creates encumbrances from requisitions, purchase orders and other transactions originating in feeder systems such as Purchasing and Payables.

When you do not enable the budgetary control flag, you can still enter manual encumbrances via journal entry, but you cannot generate encumbrances from requisitions and purchase orders. You have two options for using encumbrance data to monitor over–expenditure of a budget: After actuals and encumbrances have been posted, you can generate reports to show over–expenditures. You can also use funds checking to prevent over–expenditures before they occur.

The following figure shows the encumbrance accounting process with the budgetary control flag enabled.

In business, an encumbrance is created when a Purchase Order is issued to buy goods or services. The money has not yet been spent, but is "earmarked" for that purchase and no one else can use it. In real life, if you put money into an envelope to hold it to pay a bill, you have encumbered that money. You probably don’t use budget codes, but if you have an envelope in your dresser drawer marked “ELECTRIC BILL”, the money you stash away for the next bill is your encumbrance. How much should be encumbered? How much do you THINK your bill is going to be? That’s the encumbrance.

The primary purpose of tracking encumbrances is to avoid overspending a budget. Encumbrances can also be used to predict cash outflow and as a general planning tool.

To use the full capabilities of encumbrance accounting, you must enable the budgetary control flag for a set of books. When you enable the budgetary control flag, the system automatically creates encumbrances from requisitions, purchase orders and other transactions originating in feeder systems such as Purchasing and Payables.

When you do not enable the budgetary control flag, you can still enter manual encumbrances via journal entry, but you cannot generate encumbrances from requisitions and purchase orders. You have two options for using encumbrance data to monitor over–expenditure of a budget: After actuals and encumbrances have been posted, you can generate reports to show over–expenditures. You can also use funds checking to prevent over–expenditures before they occur.

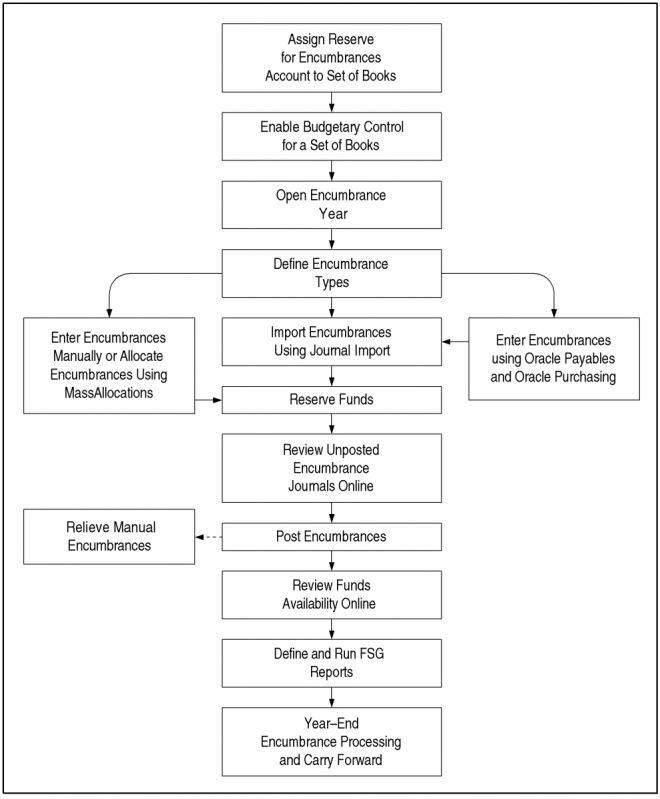

The following figure shows the encumbrance accounting process with the budgetary control flag enabled.

0 comments